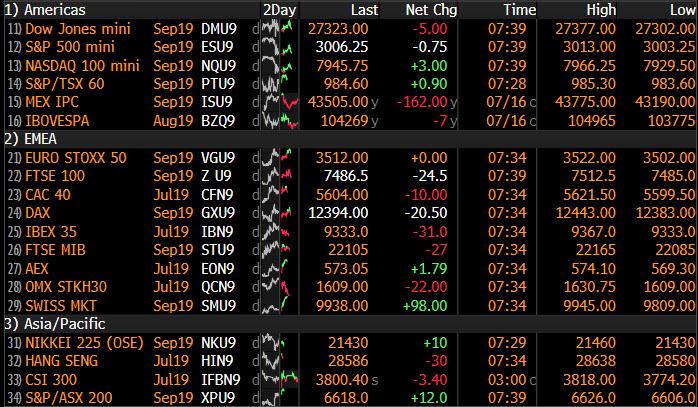

US equity futures gave up some of their earlier (low-volume) gains after Bank of America’s net interest income fell short of analysts’ expectations, though CEO Brian Moynihan said the economy appeared to be improving. The Stoxx Europe 600 index nudged higher amid a mixed bag of reports from companies including Swatch, Ericsson and ASML. In the US, earnings from the big banks JPMorgan, Citigroup and Wells Fargo this week have raised concerns that lower interest rates will pressure profits at a time when revenue growth is already slow.

Adding some nervousness to markets was a threat from U.S. President Donald Trump to tax another $325 billion worth of Chinese goods. And in the latest evidence that trade tensions were hurting businesses, railroad CSX reported a quarterly profit that missed estimates and lowered its full-year revenue forecast, sending its shares 7.2% lower. Also worth noting, on Tuesday more dovish comments from Federal Reserve Chairman Jerome Powell did little to stir markets, suggesting easing may be fully priced in as Bloomberg points out.

Meanwhile, in Europe, strong quarterly profit from Dutch chip equipment maker ASML helped semiconductor makers including Advanced Micro Devices, Micron Technology, Intel and Applied Materials rise between 0.4% and 1.6%. Qualcomm jumped 5.6% after the U.S. Justice Department asked a federal appeals court to pause the enforcement of a sweeping antitrust ruling against the mobile chip supplier.

Earlier in the session, Asian stocks slipped for a second day, with South Korean shares leading declines amid regional and global trade tensions. Technology and energy were among the weakest sectors after U.S. President Donald Trump reiterated that he could impose additional tariffs on Chinese imports if he wants. Most markets in the region dropped, while Australia bucked the trend with the S&P/ASX 200 gauge up 0.5%, supported by BHP Group after the miner forecast iron ore production will rise as much as 6% this fiscal year. China’s Shanghai Composite Index fell as large financial companies led losses. The Kospi retreated 0.9%, dragged by Samsung Electronics and SK Hynix, while the Topix closed 0.1% lower. India’s Sensex added 0.2%, with Kotak Mahindra Bank and Infosys among the biggest boosts, as investors awaited more corporate earnings.

In FX, the dollar halted a two-day rally, held down by gains in commodity currencies, with the Canadian dollar rallying ahead of inflation data. Even so, it held near its strongest level in a week as traders awaited economic data and speeches by Federal Reserve officials in coming days for clues about the size of expected interest-rate cuts this year. The pound traded near the lowest levels since April 2017 as the risk of a no-deal Brexit continued to preoccupy investors.

Elsewhere, Bitcoin extended a slide below $10,000.

In commodities, WTI and Brent futures are nursing some of yesterday’s losses after prices slid around 3% on comments from the US which suggested a tempering of US-Iran tensions, albeit this was later rebutted by Iran. Upside for the complex has been limited by a number of supply-side factors including the narrower-than-expected drawdown in API crude stocks (-1.4mln vs. Exp. -2.7mln). Furthermore, refineries in the Gulf are restarting operations post-storm Barry, with only 59% of production still offline (vs. 69% on Monday).

Elsewhere, gold prices are gravitating closer to the key 1400/oz mark as the Dollar index gains more ground above 97.00. Meanwhile, Dalian iron ore futures have retreated from recent record highs as investors digested news about higher transaction fees in all iron ore futures contracts on the DCE alongside a rise in iron ore shipments to China from Australia.

Expected data include housing starts and building permits. Abbott, Bank of America, IBM, and Netflix are among companies reporting earnings...

- Source, Zero Hedge, Read More Here