Illegal foreign dark money... Runaway corruption and collusion at all levels of government and banking...

Shoddy contractors perpetrating hazardous deception with impunity as crony inspectors wink and look the other way...

Olympic athletes dropping like flies in a village built over industrial toxic waste...

A real-estate bubble reaching nosebleed heights of distortion, while dragging innocent investors to their ruin, threatening thousands of residents with illness/ risk of death/ and financial failure...

A looming national banking collapse capable of triggering a global financial pandemic... Sound like the stuff of trashy paperback detective novels?

Think again: it’s not fiction, but the very real and present danger beneath one of the world’s most famous real-estate markets.

And it’s showing literal cracks ready to come crashing down on all of us. Australian investigative realtor and whistleblower Edwin Almeida visits Reluctant Preppers for the first time to break open a national scandal of easy-money fueled corruption creating a massive public health hazard and arming a financial time-bomb.

Will this threat start the collapse of the sky-high Australian real estate market, and a domino-effect of bank failures? Is this a black swan hatching as we speak?

Why are we looking at an interest rate cut as the DOW is sitting at all time highs in the longest bull market in history? Is the rate cut purely politically motivated?

The US Dollar index remains in a rising channel, nowhere near the all time highs, again begging the question as to why a rate cut is on the table?

The pound is now almost 1:1 with the US Dollar… possibly there is international pricing pressure for competitive purposes?

We look back at the last week of gold price movements alongside silver price movements in 2019. We’ll review the gold to silver ratio and platinum to palladium ratio movements.

Boris Johnson is now the British Prime Minister implies a hard Brexit later this year…

Finally a deal has been met with the federal budget, ensuring no shutdown, but raising spending levels by $320 billion above the limits previously set.

There's many examples of the Federal Reserve making bad predictions and being wrong for a long time now and it's causing panic, confusion, chaos and desperation that is building up.

It looks like we are about to get a weaker US dollar. Why is a weak dollar coming, and how can we prepare for it?

With gold? With silver? Join James Anderson and Half Dollar as they discuss several reasons for owning gold & silver, and why now is the time to get prepared.

I have always secretly wanted to work at a precious metals bullion dealer.

I love gold GC00, +0.42%. And silver and platinum. I love them philosophically, and I also just like shiny rocks. But if you think about it, trading metals is a really weird business.

Say you are bullish on silver and want to speculate on it, thinking it will appreciate in price. You can buy an ETF, yes, or you can buy silver miners, but the most straightforward way to invest in silver is just to buy coins or bars.

The most popular coins come from the U.S. Mint, but you can get coins from other countries, too. The most popular silver bars for retail investors are the 100-ounce bars, which are typically manufactured by one of a few silver refiners. Asahi is the new standard, after Johnson Matthey sold its gold and silver refining operations to them.

Anyway, you can go to a bullion dealer, tell them you want a 100-ounce bar, and they will charge you the spot price of silver per ounce, times 100 ounces, plus a small markup.

So you buy it, and now you have a shiny rock. It is satisfying to have shiny rocks, especially the 100-ounce silver bars, which make you feel like a baller.

But the shiny rocks don’t do anything. You aren’t going to use them to sew a button, wash your car or paint your ceiling. They just sit there. You hold them for a while, and if the price goes up, you are supposed to sell them.

But most people don’t sell them, and then the price goes back down, and they end up in an estate sale, and the dealer buys them back at a discount. Paraphrasing Warren Buffett, someone watching from Mars would be scratching their heads. There really is nothing more useless in the world than a shiny rock. But we love ’em...

Jason received more information about China's real estate bubble from one of his mainland China sources including some anecdotes about how owners of houses don't want renters.

Ronald discusses the potential for trust problems within the banking system and why these types of issues can happen quite quickly. His annual report "In Gold we Trust" looks at the problems looming in the financial sector.

Trust in the political system, media, and science all appear to be crumbling at the moment. However, trust in the economy and the U.S. dollar remains reasonably stable.

A monetary u-turn is coming, which will likely bring a recession to many countries. What will central banks do to mitigate this, and it seems likely they will counter this with more quantitative easing.

Both silver and gold have seen a strong week as silver now sits above $16.20 and gold rests at $1440.00. Learn how the price movements of the white metals have impacted ratio opportunities for precious metals investors.

We will cover the price movements of gold, silver, platinum, palladium, the US Dollar Index, Euro Index, and DOW in this week's Golden Rule Radio.

Macroeconomic analyst Rob Kirby lays out what is coming and says, “When the dollars start coming home, there will be inflation.

We have seen the rejection of U.S. debt, but the dollars are being recycled into other things like Bitcoin and equities. There is going to come a point where the dollars are going to come home to America, and people are going to start demanding real stuff.

I can envision a day when there might be a domestic dollar and an international dollar, and there might be two values assigned to the domestic and international dollar.

Whether this happens or not, the purchasing power of the dollar is going to be diminished as the story about the “missing” $21 trillion gains traction around the world.”

LAST year, 22 central banks, situated largely to the east of Germany, bought the largest amount of gold since 1967 - the year that the London Gold Pool collapsed. The gold repatriations by many European countries in the last few years are another sign that we are reaching the end of four decades of monetary calm. This could bring about the largest monetary changes since the closing of the gold window by US President Richard Nixon in 1971.

The US wants its fiat dollar system to prevail for as long as possible. It has every interest in preventing a "rush out of dollars towards gold", as happened in the 1970s. Since then, bankers have tried to exercise control over the precious metal's price. This war on gold has been ongoing for almost 100 years, but gained traction in the 1960s with the forming of the London Gold Pool - whose members included the US, UK, Netherlands, Germany, France, Italy, Belgium and Switzerland.

During meetings of central bank chiefs at the Bank for International Settlements in 1961, the eight participating countries agreed to make available a gold pool worth US$270 million. This was focused on preventing the gold price from rising above US$35 per troy ounce, as set during Bretton Woods, by selling official gold holdings from the central banks' gold vaults.

However, in March 1968, the pool was disbanded because France would no longer cooperate. This signalled the start of a 13-year "bull market" and sent gold to more than US$800 per troy ounce in 1980.

Today, Washington may consider it useful to bring back gold to support the US dollar. Some US insiders have even called openly for a return to the old way of doing things. Neo-conservative Robert Zoellick, the former president of the World Bank, wrote an open letter to the Financial Times in 2010 entitled "Bring back the gold standard".

A 2012 study by the Chatham House gold task force suggested that the metal could be added to the International Monetary Fund's special drawing right (SDR). One of the members of this task force was Lord Meghnad Desai, chair of the Official Monetary and Financial Institutions Forum (OMFIF) advisers council. During a conference in Dubai he remarked: "We could ask that gold be nominated as part of the SDR. That is one thing I think is quite likely to happen. This will be easier if China increases its official gold holdings."

Beijing wants to increase its gold reserves in the shortest time possible to at least 8,000 tonnes. This would put China on a par, in terms of its gold to gross domestic product (GDP) ratio, with the US and European Union. It would open the way, should the need arise, for a possible joint US-EU-China gold revaluation to support the financial system.

Beijing must realize that the US could surprise the world with a unilateral gold revaluation. Wikileaks revealed a cable, sent in early 2010 to Washington from the US embassy in Beijing, which quoted a Chinese news report about the consequences of such a US dollar devaluation: "If we use all of our foreign exchange reserves to buy US Treasury bonds, then when someday the Federal Reserve suddenly announces that the original 10 old dollars are now worth only one new dollar, and the new dollar is pegged to the gold - we will be dumbfounded."

In recent years, there have been numerous statements demonstrating China's understanding of the "dark forces" suppressing the price of gold on Wall Street. Zhou Xiaochuan, then-governor of the People's Bank of China, revealed in a 2009 article that the Chinese recognize the hypocrisy of US policy towards gold: "After the disintegration of the Bretton Woods system in the 1970s, the gold standard - which had been in use for a century - collapsed. Under the influence of the dollar hegemony, the stabilizing effect of gold was widely questioned; the 'gold is useless' discussion began to spread around the globe . . . Currently, there are more and more people recognizing that the 'gold is useless' story contains too many lies. Gold now suffers from a 'smokescreen' designed by the US, which stores 74 per cent of global official gold reserves, to put down other currencies and maintain the dollar hegemony." Since then, China and Russia have stopped buying US Treasuries while adding physical gold reserves.

Clearly, gold is making a remarkable comeback to the world financial system. A new gold standard is being born without any formal decision. At least, that is how Ambrose Evans-Pritchard, an influential international business editor of The Telegraph, described the ongoing efforts by countries to lay their hands on physical gold: "The world is moving step by step towards a de facto gold standard, without any meetings of G-20 leaders to announce this." OMFIF

How can I not talk about the Fed? How can I not talk about the daily jawboning? It is all around us. Every. Single. Day.

And it keeps working.

I feel like I’m being reduced to a loon conspiracy theorist documenting the very reality of it. But I’m not. From my perch I’m doing a public service doing it, because the background motivation for why it is being done reveals a deeper and disturbing truth: They are scared, they are worried and they are desperate to keep the balls in the air.

In my view it’s disingenuous to not acknowledge the real impact central banks have on markets and assess the risk implications.

Yesterday the Fed went full circus. It was stunning to watch and I suspect they made a couple of mistakes by revealing things they shouldn’t have.

Not a surprise Bullard wants to see cuts, but it was Clarida and Williams who dropped the bombs. Wait for bad data? Nah, just cut preemptively. A full abandonment of the ‘data dependency’ charade. To ‘influence markets’. Stated straight up for all to see. They are no longer even pretending.

And a stunning admission from Williams: “When you only have so much stimulus at your disposal, it pays to act quickly to lower rates at the first sign of economic distress.”

It pays to act when you have limited ammunition. A clear acknowledgement of what I’ve been outlining: The Fed, by not being being able to normalize in this cycle, is scrapping at the bottom.

So they want to intervene before things turn bad and hope this will prevent a recession. How? By blowing the asset bubble even higher.

And it worked again yesterday. Stocks flew higher, especially in after hours.

But then the New York Fed came and sheepishly claimed Williams didn’t really mean it, he was just speaking theoretically wink, wink, don’t you know.

Oh please. Nobody believes you. While futures dipped momentarily on the clarification the monkeys came back and bid stocks back up in classic magic risk free Friday fashion.

My take here for what it’s worth? This week economic data actually showed strength in the economy which is paradoxically what the Fed didn’t want to see as it weakened the argument for rate cuts in July. Stocks took the cue and sold off and the 3,000 level was gone, wedge patterns were breaking and we were at the cusp of a failed breakout after tagging the major trend lines.

So if the data kills your rate cut argument what do you do? You declare the data irrelevant and ramp up expectations for a rate cut anyways and jam stocks higher again and save pattern breaks.

Yes it is this banal, but this is precisely what happened and we can see it in the charts.

And there it is:

On Wednesday odds for a 50bp rate cut had dropped to 34%, by the time Clarida, Bullard, and Williams were done these odds had skyrocketed to 71%.

Come on. None of this is an accident.

JP Morgan now expects 12 central banks to cut rates in the next 2 months. The global easing cycle has begun. With negative rates still in place.

What’s all this really tell us? A recession is coming, they know it and they are desperate to prevent it. It also says zero rates are coming back and I suspect, in due time, negative rates. Which means markets will eventually drop despite the current efforts to jam things higher.

But a Fed desperate to jawbone markets higher, to “influence markets” is playing the most dangerous game.

A Fed admitting they have limited ammunition and are openly abandoning their data dependency mantra to stop the business cycle is an open admission of weakness. And a weak Fed may commit the worst sin a Fed can commit: Lose confidence of the market...

How we're constantly at war with our biological programming.

"Until you make the unconscious conscious, it will direct your life and you will call it fate". ~ Carl Jung

I love that Jung quote.

I’ve used it generously in conversation, seminars and writings throughout the years.

Initially, I assumed that the “unconscious” he referred to the place in our brains where our experiences, beliefs and memories are undetectably stored.

You know, psychology stuff: ego, subconscious, id. Old memories from childhood lurking beneath the conscious frame of reference, directing thoughts and coloring our current experiences."

Buffett became a billionaire on paper when Berkshire Hathaway began selling class A shares on May 29, 1990, when the market closed at $7,175 a share.

In 1998, in an unusual move, he acquired General Re (Gen Re) for stock. In 2002, Buffett became involved with Maurice R. Greenberg at AIG, with General Re providing reinsurance.

On March 15, 2005, AIG's board forced Greenberg to resign from his post as Chairman and CEO under the shadow of criticism from Eliot Spitzer, former attorney general of the state of New York. On February 9, 2006, AIG and the New York State Attorney General's office agreed to a settlement in which AIG would pay a fine of $1.6 billion.

In 2010, the federal government settled with Berkshire Hathaway for $92 million in return for the firm avoiding prosecution in an AIG fraud scheme, and undergoing 'corporate governance concessions'. In 2002, Buffett entered in $11 billion worth of forward contracts to deliver U.S. dollars against other currencies.

By April 2006, his total gain on these contracts was over $2 billion. In 2006, Buffett announced in June that he gradually would give away 85% of his Berkshire holdings to five foundations in annual gifts of stock, starting in July 2006.

The largest contribution would go to the Bill and Melinda Gates Foundation. In 2007, in a letter to shareholders, Buffett announced that he was looking for a younger successor, or perhaps successors, to run his investment business.

Buffett had previously selected Lou Simpson, who runs investments at Geico, to fill that role.

However, Simpson is only six years younger than Buffett. Buffett ran into criticism during the subprime crisis of 2007--2008, part of the late 2000s recession, that he had allocated capital too early resulting in suboptimal deals. "Buy American. I am." he wrote for an opinion piece published in the New York Times in 2008.

Buffett has called the 2007--present downturn in the financial sector "poetic justice". Buffett's Berkshire Hathaway suffered a 77% drop in earnings during Q3 2008 and several of his recent deals appear to be running into large mark-to-market losses. Berkshire Hathaway acquired 10% perpetual preferred stock of Goldman Sachs.

Some of Buffett's Index put options (European exercise at expiry only) that he wrote (sold) are currently running around $6.73 billion mark-to-market losses.

The scale of the potential loss prompted the SEC to demand that Berkshire produce, "a more robust disclosure" of factors used to value the contracts. Buffett also helped Dow Chemical pay for its $18.8 billion takeover of Rohm & Haas.

He thus became the single largest shareholder in the enlarged group with his Berkshire Hathaway, which provided $3 billion, underlining his instrumental role during the current crisis in debt and equity markets.

In 2008, Buffett became the richest man in the world, with a total net worth estimated at $62 billion by Forbes and at $58 billion by Yahoo, dethroning Bill Gates, who had been number one on the Forbes list for 13 consecutive years.

In 2009, Gates regained the position of number one on the Forbes list, with Buffett second.

Their values have dropped to $40 billion and $37 billion, respectively, Buffett having lost $25 billion in 12 months during 2008/2009, according to Forbes.

In October 2008, the media reported that Warren Buffett had agreed to buy General Electric (GE) preferred stock.

The operation included extra special incentives: he received an option to buy 3 billion GE at $22.25 in the next five years, and also received a 10% dividend (callable within three years).

In February 2009, Buffett sold some of the Procter & Gamble Co, and Johnson & Johnson shares from his portfolio...

The appointment of Christine Lagarde as president of the ECB has been greeted with euphoria by financial markets. That reaction in itself should be a warning signal. When risky assets soar in the middle of a huge bubble due to a central bank appointment, the supervising entity should be concerned.

Lagarde is a lawyer, not an economist, and a great professional, but the market probably interprets correctly that the European Central Bank will become even more dovish. Lagarde, for example, is a strong advocate of negative rates.

Lagarde and Vice President De Guindos have warned of the need to carry out measures to avoid a possible financial crisis, proposing different mechanisms to mitigate the shocks created by excess risk. Both are right, but that search for mechanisms to work as shock buffers runs the risk of being sterile when it is the monetary policy that encourages excess. When the central bank solves a financial crisis by absorbing the excess risk that the market once took it does not reduce it, it only disguises it.

Supervisors ignore the effect of risk accumulation because they perceive it as necessary collateral damage to the recovery. Risk accumulates precisely because it is encouraged.

Draghi said that monetary policy is not the correct instrument to deal with financial imbalances and macroprudential tools should be used. However, it is the monetary policy which is causing those imbalances when an extraordinary, conditional, and limited measure becomes an eternal and unconditional one.

When monetary policy disguises and encourages risk, macroprudential measures are simply ineffective. There is no macroprudential measure that mitigates the risk created by negative rates and almost three trillion of asset purchases. More than half of European debt has negative returns and the ECB must maintain the repurchase of maturities, injections of liquidity, and even announce a new program of quantitative easing in the face of the lack of sufficient demand in the secondary market for those negative yielding bonds. That is a bubble.

Risk builds up slowly and happens instantaneously. That is what the central planner does not seem to want to understand and the reason why stress tests and macroprudential measures fail in the midst of monetary stimuli. Because they start from a fallacious base: Ceteris paribus and that the already accumulated imbalances are manageable.

When most eurozone countries finance themselves at negative rates for up to seven to ten years, there is no reason to maintain current rates and stimuli.

The central planner can say that bond yields are low due to market demand, but when the Central Bank supplants the market by injecting, repurchasing maturities, and announcing more monetary stimuli, the placebo effect in the real economy is imperceptible and the risk in financial assets is huge. The huge injection of the money supply goes to other risk assets in search of a diminishing yield.

The eurozone has been in stagnation for several months, with many leading indicators worsening, and it is not due to lack of stimulus, but due to excess.

64% of the sovereign debt of the eurozone hs negative yields. Five trillion euros. Completely unjustified looking at solvency, liquidity, or growth ratios.

Junk bonds are at the lowest yield in thirty years, while the rating agencies warn that the solvency and liquidity ratios have not improved. The BIS warned of the increase of zombie companies, eternally refinanced at low rates despite not being able to cover their interest expenses with operating profit. Meanwhile, companies on the verge of bankruptcy are financed at rates of 3.5-4%.

The multiples paid for infrastructure assets have soared in little more than half a decade and now no one is surprised to see 19 times EBITDA paid for assets driven by low rates and cheap debt.

Excess liquidity reached 1.2 trillion euros. It has multiplied sevenfold since the launch of the repurchase program.

The debt of non-financial companies in the eurozone remains above 78% of GDP, according to Standard and Poor’s, above the cycle maximum of the fourth quarter of 2008.

Many say that nothing has happened yet, although it is more than debatable, according to bankruptcies of financial entities and increase of zombie companies. However, the fact that there has not been a massive financial crisis yet does not mean that the bubble is not being inflated. And when that bubble is in several assets at once, there are no macroprudential measures to cover the risk.

The problem of central planners is one of diagnosis. They think that if credit does not grow as much as they think it should grow and investment and growth are not what they estimated, it is because more stimulus is needed. Many ignore the effect of overcapacity, excess debt and demographics while carrying out the greatest transfer of wealth from savers and the productive economy to the indebted.

Calls for prudence and risk analysis measures would be much more effective if misallocation of capital was not encouraged by the policy itself. We must be aware that lower rates and more liquidity will not improve the economy, but they may generate a dangerous boomerang effect on risk assets.

Lagarde faces two difficult options. On one side, continue with negative rates and liquidity injections which perpetuate overcapacity, make governments avoid structural reforms, and stagnate the economy. On the other side, normalizing monetary policy would show the artificially low yields of sovereign debt as unsustainable. She needs to face reality. The eurozone does not need more monetary stimulus or government spending, it needs less interventionism.

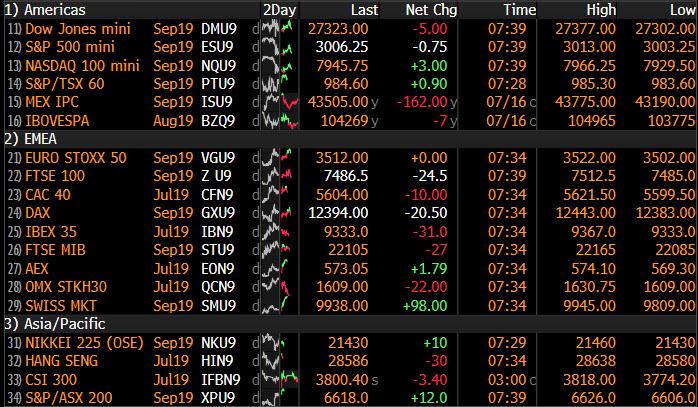

S&P futures pared gains, and traded unchanged as mixed Q2 earnings and disappointing hints by banks on future revenue gave traders concerns about the sustainability of the rally, while European stocks struggled for traction amid fresh trade tensions.

US equity futures gave up some of their earlier (low-volume) gains after Bank of America’s net interest income fell short of analysts’ expectations, though CEO Brian Moynihan said the economy appeared to be improving. The Stoxx Europe 600 index nudged higher amid a mixed bag of reports from companies including Swatch, Ericsson and ASML. In the US, earnings from the big banks JPMorgan, Citigroup and Wells Fargo this week have raised concerns that lower interest rates will pressure profits at a time when revenue growth is already slow.

Adding some nervousness to markets was a threat from U.S. President Donald Trump to tax another $325 billion worth of Chinese goods. And in the latest evidence that trade tensions were hurting businesses, railroad CSX reported a quarterly profit that missed estimates and lowered its full-year revenue forecast, sending its shares 7.2% lower. Also worth noting, on Tuesday more dovish comments from Federal Reserve Chairman Jerome Powell did little to stir markets, suggesting easing may be fully priced in as Bloomberg points out.

Meanwhile, in Europe, strong quarterly profit from Dutch chip equipment maker ASML helped semiconductor makers including Advanced Micro Devices, Micron Technology, Intel and Applied Materials rise between 0.4% and 1.6%. Qualcomm jumped 5.6% after the U.S. Justice Department asked a federal appeals court to pause the enforcement of a sweeping antitrust ruling against the mobile chip supplier.

Earlier in the session, Asian stocks slipped for a second day, with South Korean shares leading declines amid regional and global trade tensions. Technology and energy were among the weakest sectors after U.S. President Donald Trump reiterated that he could impose additional tariffs on Chinese imports if he wants. Most markets in the region dropped, while Australia bucked the trend with the S&P/ASX 200 gauge up 0.5%, supported by BHP Group after the miner forecast iron ore production will rise as much as 6% this fiscal year. China’s Shanghai Composite Index fell as large financial companies led losses. The Kospi retreated 0.9%, dragged by Samsung Electronics and SK Hynix, while the Topix closed 0.1% lower. India’s Sensex added 0.2%, with Kotak Mahindra Bank and Infosys among the biggest boosts, as investors awaited more corporate earnings.

In FX, the dollar halted a two-day rally, held down by gains in commodity currencies, with the Canadian dollar rallying ahead of inflation data. Even so, it held near its strongest level in a week as traders awaited economic data and speeches by Federal Reserve officials in coming days for clues about the size of expected interest-rate cuts this year. The pound traded near the lowest levels since April 2017 as the risk of a no-deal Brexit continued to preoccupy investors.

Elsewhere, Bitcoin extended a slide below $10,000.

In commodities, WTI and Brent futures are nursing some of yesterday’s losses after prices slid around 3% on comments from the US which suggested a tempering of US-Iran tensions, albeit this was later rebutted by Iran. Upside for the complex has been limited by a number of supply-side factors including the narrower-than-expected drawdown in API crude stocks (-1.4mln vs. Exp. -2.7mln). Furthermore, refineries in the Gulf are restarting operations post-storm Barry, with only 59% of production still offline (vs. 69% on Monday).

Elsewhere, gold prices are gravitating closer to the key 1400/oz mark as the Dollar index gains more ground above 97.00. Meanwhile, Dalian iron ore futures have retreated from recent record highs as investors digested news about higher transaction fees in all iron ore futures contracts on the DCE alongside a rise in iron ore shipments to China from Australia.

Expected data include housing starts and building permits. Abbott, Bank of America, IBM, and Netflix are among companies reporting earnings...

On October 29, 1929, Black Tuesday hit Wall Street as investors traded some 16 million shares on the New York Stock Exchange in a single day.

Billions of dollars were lost, wiping out thousands of investors. In the aftermath of Black Tuesday, America and the rest of the industrialized world spiraled downward into the Great Depression (1929-39), the deepest and longest-lasting economic downturn in the history of the Western industrialized world up to that time.

1929 Stock Market Crash During the 1920s, the U.S. stock market underwent rapid expansion, reaching its peak in August 1929, after a period of wild speculation.

By then, production had already declined and unemployment had risen, leaving stocks in great excess of their real value.

Among the other causes of the eventual market collapse were low wages, the proliferation of debt, a struggling agricultural sector and an excess of large bank loans that could not be liquidated. Stock prices began to decline in September and early October 1929, and on October 18 the fall began.

Panic set in, and on October 24, Black Thursday, a record 12,894,650 shares were traded. Investment companies and leading bankers attempted to stabilize the market by buying up great blocks of stock, producing a moderate rally on Friday.

On Monday, however, the storm broke anew, and the market went into free fall. Black Monday was followed by Black Tuesday (October 29), in which stock prices collapsed completely and 16,410,030 shares were traded on the New York Stock Exchange in a single day.

Billions of dollars were lost, wiping out thousands of investors, and stock tickers ran hours behind because the machinery could not handle the tremendous volume of trading.

1929 Stock Market Crash and the Great Depression After October 29, 1929, stock prices had nowhere to go but up, so there was considerable recovery during succeeding weeks.

Overall, however, prices continued to drop as the United States slumped into the Great Depression, and by 1932 stocks were worth only about 20 percent of their value in the summer of 1929.

The stock market crash of 1929 was not the sole cause of the Great Depression, but it did act to accelerate the global economic collapse of which it was also a symptom.

By 1933, nearly half of America’s banks had failed, and unemployment was approaching 15 million people, or 30 percent of the workforce.

With all the white noise on July 4th - tanks and flyovers, speeches - it can be easy to forget exactly what we are celebrating. In this special edition of the Liberty Report, Ron Paul explains his favorite part of the Declaration and why...

Silver is a bargain compared to gold, and things look bullish for both metals, this according to Lobo Tiggre, principal analyst of the Independent Speculator.

“Where gold goes, silver follows, and the fact is it’s still relatively cheap,” Tiggre told Kitco News. “I absolutely have silver plays at the very top of my research list.”

On the asteroid 16 Psyche, Tiggre said that much of the asteroid is composed of iron, so reports of an asteroid made of gold that could contain enough wealth to make everyone on the planet billionaires is “silly.”

David McAlvany, President of the McAlvany Financial Companies, explains his view for a weaker dollar and how it affects the markets, gold and commodities.

A needed mindset for the age we live in. "We didn’t have a lot growing up, as my mom had to single-parent three kids. Most anything I wanted required disciplined frugality.

I bought my first fly rod from Orvis at the age of 13, which took the better part of a year to save up for. I hand-tied the first flies drifted from its lines from the hackles of roosters I raised expressly for that purpose."

Why we may soon see prices of $1,500-1,600/oz Fresh from releasing his exhaustive 340-page annual report titled In Gold We Trust, Ronald Stoerferle joins us to summarize his forecast for the yellow metal. Stoerferle, an author of several books on Austrian economics and head of strategy and portfolio management at Incrementum AG, concludes that gold is poised to move explosively higher. He sees a new bull market beginning for the precious metal — one likely to quickly build momentum as the impending recession arrives and the world’s central banks revert to extreme easing policy measures. - Source, Reluctant Preppers

The Federal Reserve and markets are intensely focused on discussion among world leaders during the Group of 20 summit in Japan as what unfolds will influence the outcome of the global economy, according to Chris Versace, chief investment officer at Tematica Research.

“It’s a binary outcome,” he said. “Either trade talks are back on and we’re going to work towards a deal, or things didn’t go well and President Trump is going to go forward with that next round of tariffs.”

Versace stressed that although expectations are high that the Fed will reduce rates in their meeting next month, what happens in the summit will have an effect on their decision.

“If we come out of this and trade talks are still in process, that means the existing tariffs are still on,” he said. “I think investors are going to get nervous about the expectations for the back-half of the year.”