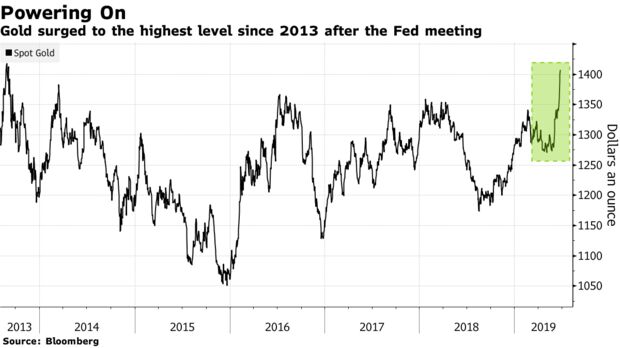

Emerging from a 6-year base, gold shows signs that money is flowing into the precious metal in a big way, vaulting past the $1,350 barrier, and testing higher resistance and support limits.

What mega-factors are driving this surge in gold, and what further monetary development may be about to become the biggest financial event of the year that could amplify these trends?

Market analyst and founder of WealthResearchGroup.com, Lior Gantz, returns to ReluctantPreppers to assert that we can layer our financial fortress to protect against risk & loss, provide for real growth, and be aware of many different options for outsized opportunities that are developing now.

Gold’s rally to the highest since 2013 may have room to run further after the Federal Reserve indicated a readiness to cut borrowing costs, which would keep real rates low and weigh on the dollar, according to BlackRock Inc.

“Gold could end the year higher,” Russ Koesterich, portfolio manager at the $27 billion BlackRock Global Allocation Fund, said in an interview. “If we continue to see a pivot toward easier monetary policy from the Fed, then I think gold can go higher from here,” he said, adding that there is likely to be some pullback and consolidation in the near-term.

Gold is back in the limelight as investors seek havens amid slowing global growth due to the fallout from the U.S.-China trade dispute and as central banks globally adopt a more dovish tone. While the Fed left its key rate unchanged on Wednesday, it dropped a reference to being “patient” on borrowing costs and forecast a larger miss of their 2% inflation target this year. The greenback weakened to erase its 2019 gains.

“If easier policy from the Fed contains the dollar, that’s an environment, all else equal, that is supportive of gold,” Koesterich said last week in a phone interview after the central bank’s decision. “What I’d add is if we get a situation where the Fed is easing perhaps more than people thought because trade frictions are rising, that might be a particularly strong period for gold.”

The Fed would be easing at the same time as volatility would be rising and demand from investors for hedges would be going up, he said.

Spot gold rose as much as 0.8% to $1,411.23 an ounce and traded at $1,406.02 at 7:12 a.m. in London. Prices surged to $1,411.63 on Friday, the highest level in more than five years. Citigroup Inc. said Thursday that the enthusiasm is justified, with $1,500 to $1,600 possible in the next 12 months under a bullish-case scenario that includes borrowing costs falling below zero.

The Fed last cut rates in 2008 and began its most recent tightening cycle at the end of 2015, with four hikes last year. The so-called dot plot, which the U.S. central bank uses to signal its outlook for the path of interest rates, shows that policy makers are divided for the remainder of 2019. European Central Bank President Mario Draghi last week paved the way for a rate cut, and counterparts in Australia, India and Russia have lowered borrowing costs.

“In the near term, gold, like bonds, has had a very large move, so it would not be surprising if there was some consolidation,” said Koesterich, adding that BlackRock’s bullion holdings through exchange-traded funds have been “relatively static” over the last month. “But if we are moving into a period where the Fed or other central banks feel the need to ease monetary conditions, gold is probably going to have a better environment than it did earlier this year.”

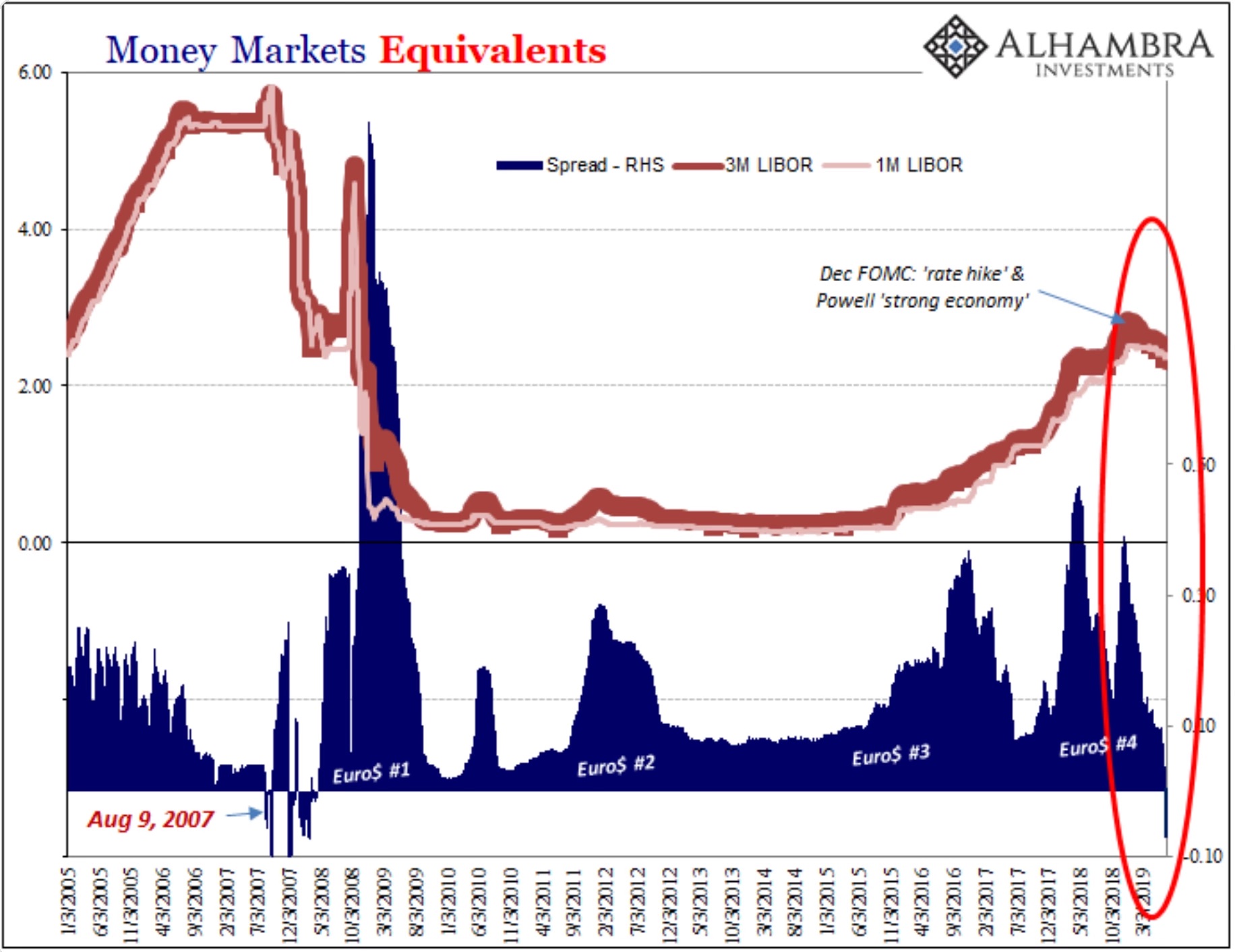

Jeff Snider from Alhambra Partners: “LIBOR curve inverts for first time since 2008 (doesn’t mean we are repeating 2008, just that the negative risks are substantial). (See chart below).

Risks In The Global Financial System Are Now Substantial

Remember Gold?

Andrew Adams from Raymond James: “Gold has received a lot of attention lately, as it has finally done something after about seven years of drifting sideways. I wouldn’t want to chase it here, but it does look like an inflection point has been reached where dips are for buying. The metal has put in higher lows since late 2015 and if it does drop down closer to $1375-$1400 I think it would be worth taking a chance on. (See chart below).

Pullbacks In Gold Are Now Buying Opportunities

Weaker Dollar Helping Commodity Prices Too

Andrew Adams from Raymond James continues: “President Trump seems to be getting his wish for a weaker U.S. dollar, as the U.S. Dollar Index has fallen over the last week to break the uptrend that had been in place since last year. This is helping commodities like Gold and Oil priced in dollars...

Even if the U.S. and China come to some sort of an agreement at this week’s G-20 summit, the world’s two largest economies will still be fighting for much longer, conservative economics writer Stephen Moore told CNBC on Wednesday.

“This trade dispute isn’t going to be solved in the next year or two. This is going to be the epic battle of our times,” said Moore, who withdrew his name from President Donald Trump’s consideration in May for a nomination to the Federal Reserve Board. “It’s going to go on for 10 or 15 years.”

Washington and Beijing have been engaged in a trade war for nearly a year, and the two countries have stepped up retaliatory efforts on one another in the past month.

Trump and President Xi Jinping are set to meet at the G-20 summit on Saturday after trade talks stalled. Treasury Secretary Steven Mnuchin told CNBC earlier Wednesday he’s confident that the U.S. and China can come to an agreement.

“We were about 90% of the way there [with a deal] and I think there’s a path to complete this,” Mnuchin told CNBC’s Hadley Gamble in Manama, Bahrain.

However, the two nations still haven’t reached an end goal and there’s a chance negotiations could fail. Moore, chief economist for the Heritage Foundation, stressed that there’s a difference between reaching a deal and almost reaching a deal.

“That’s what tripped them up last time,” Moore said. “I wouldn’t overreact to it,” referring to Mnuchin’s comments.

But if positive news comes out of this week’s trade talks, Moore said he expects the economy and U.S. markets to rise, with the Dow possibly reaching 30,000 points — it currently sits just above 26,500 points.

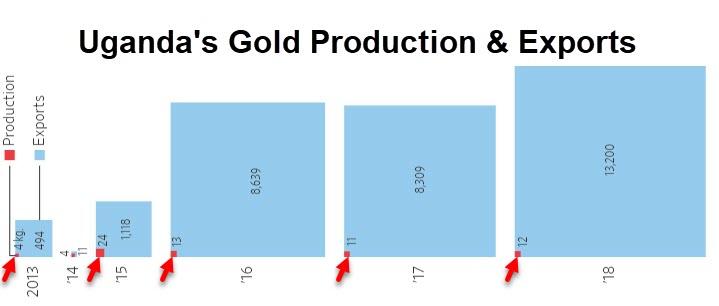

Back in March, a Uganda-based gold refinery was caught importing a massive 7.4 million tons of gold under questionable circumstances.

At the time, no one could prove definitively that it was Venezuelan gold from the Maduro regime, and half of it had already been lost to export.

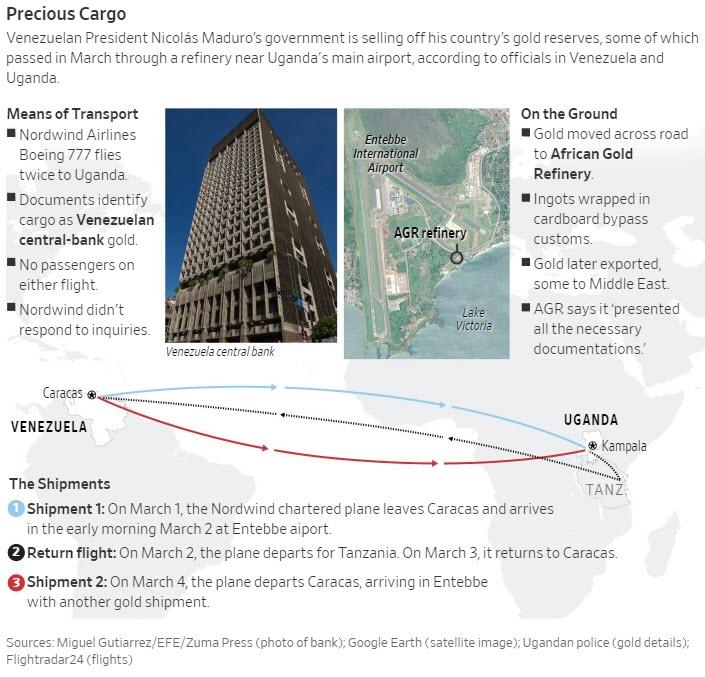

Now, a Wall Street Journalinvestigation has definitively exposed the scheme, concluding that the suspect African gold Refinery--launched by a Belgian in Uganda--is behind the operation to secretly help Maduro get the country’s gold to the market.

The investigation, citing unnamed sources close to the operation and both Venezuelan and Ugandan officials, determined that the $300 million in gold that landed in Uganda in March was transported to Uganda via Russian charter jets.

The gold landed in Entebbe, Uganda, and then went to the African Gold Refinery (AGR) before it was exported onward, according to the WSJ. The gold landed in two separate shipments of 3.8 tons and 3.6 tons.

The first shipment of 3.8 tons was exported to Turkey, based on the results of the investigation. However, the founder of AGR, Belgian businessman Alain Goetz--a big name in the African gold trade--claims that the gold was sent to Goetz Gold in Dubai, and was not exported to Turkey.

This isn’t AGR’s first flirtation with the underground economy: It’s been on the Ugandan authorities’ radar for years, including for allegedly smuggling ‘conflict gold’ from Congo and other African venues. And that gold ends up in the supply chains of major Western companies. AGR denies all of these allegations, and also says that as of March 26th, its management has agreed to steer clear of Venezuelan gold.

In the meantime, Venezuelans are suffering beyond imagination, with Maduro blaming an economic war waged he says is being waged by the U.S. and its allies, while the opposition blames Maduro’s misguided economic policies, corruption and gross mismanagement.

The Central Bank’s gold is clearly being mismanaged.

Not only do we have the regime siphoning off gold through Uganda, but Citibank and Deutsche Bank have assumed control of some $1.4 billion in Venezuelan gold. They’re holding it as a guarantee for loans, thanks to U.S. sanctions on the country’s central bank, according to Reuters.

Venezuela defaulted on a $750-million gold swap agreement with Deutsche Bank. The agreement was struck in 2016 and Venezuela put up 20 tons of gold as collateral. But interest payments were missed.

Venezuela’s opposition may not survive the fleecing of the country unscathed, either.

A separate report from the WSJ on Wednesday noted that opposition leaders are under pressure over accusations that private funds it collected from foreign governments have been embezzled.

Reports claim that millions of dollars raised for “freedom and democracy” in Venezuela were pocketed by the aides of opposition leader Juan Guaido in Colombia. Colombian spies were allegedly behind the leaking of this information. The specific funds in questions largely came from the U.S. in the form of a benefit concert organized by billionaire philanthropist Richard Branson and the money was earmarked for Venezuelan soldiers who defected to Colombia.

Which brings us back to the Uganda-Venezuela gold debacle, WSJ notes an ironic twist in the Venezuelan gold’s tale: as a person familiar with the central bank’s reserves told them: The bars almost certainly came from America in the 1940s, the person says, in payment to Venezuela for oil supplied during World War II.

A new book exposes the dark history of gold laundering in Switzerland and the modern challenge of cleaning up a lucrative industry. This is the story of the Alpine nation’s dominance over global gold trade.

Written by Swiss anti-corruption watchdog Mark Pieth, Gold Laundering – the dirty secrets of the gold trade and how to clean up shines a light on the key players in the gold industry, the different risks associated with large-scale versus artisanal mining, and the shortcomings of various international regulations and certification schemes.

How did we get here? In a discussion with swissinfo.ch, Pieth explained the history of how Switzerland came to be at the heart of a highly profitable but opaque trade. These are some of the key historical moments in the Swiss gold story, according to him.

World War II – Swiss neutrality and Nazi gold

It is a dark chapter of history for which Switzerland has not been judged kindly.

Pieth says that Switzerland benefited from its neutrality during World War II by purchasing vast amounts of gold from Allied and Axis powers. It exchanged the precious metal for Swiss francs, the only free convertible currency at the time outside the American dollar. This trade benefitted Germany in particular, effectively turning Switzerland into an enabler of the German war effort. The Swiss acquired 79% of all German gold delivered to foreign countries, with 90% of that ending up in the Swiss National Bank and the remainder in commercial banks. It is believed that Swiss banks bought CHF1.7 billion ($1.7 billion) worth of Nazi gold, including gold that Germany plundered from the reserves of conquered countries, notably Austria, Belgium, the Netherlands and Norway. Some of this gold was confiscated from private persons or removed from victims of concentration camps. After the war, the burning question was how much Switzerland knew about the gold and when. The Alpine nation agreed to pay reparations worth CHF250 million and also promised to identify dormant accounts which were heirless.

“The Swiss were the principal bankers and financial brokers of the Nazis, handling vast sums of gold and hard currency… Neutrality collided with morality; too often being neutral provided a pretext for avoiding moral considerations.” – Stuart Eizenstat, US attorney and diplomat who served as US Undersecretary of Commerce for International Trade.

Gold trade hub boosts apartheid regime in South Africa

Pieth also points out that gold trade was crucial for the survival of the South African apartheid regime. When the London Gold Pool (a gold trading hub) folded in 1968, three Swiss banks seized the opportunity to create the Zurich Gold Pool. Banks UBS, Credit Suisse and SBV (the Swiss Bank Corporation) convinced South Africa to market its production through Zurich in what became known as the “South African coup.” In addition to selling arms to South Africa, Switzerland marketed the internationally sidelined nation’s gold and diamonds. Close to 80% of the gold imported from South Africa during the 1980s was re-melted and stamped with a Swiss quality seal by refineries established by the commercial banks.

Pieth notes in his book that the former chairman of the Swiss National Bank, Fritz Leutwiler, saved South Africa from bankruptcy by helping restructure its public debt. Fear of being held to account for supporting apartheid led Switzerland to stop publishing official trade statistics on gold from 1981.

“It appears that commercial banks and officials in Switzerland were acting as gold launderers during one of the most delicate and morally dubious times in history,” concludes Pieth.

This was a crucial moment for the development of the Swiss refinery industry, he adds, as each of the three commercial banks in the Zurich Gold Pool acquired or created its own gold refinery. The practice of re-melting and re-stamping problematic gold was repeated when the Dubai-based refinery Kaloti lost its Dubai Multi Commodities Centre (DMCC) accreditation because it failed to meet sourcing standards. Refineries certified by the Swiss London Bullion Market Association (LBMA) stepped in to save the Kaloti gold.

Tapping into conflict gold amid genocide in eastern Congo

The Swiss Attorney General established in 2013 that Argor-Heraeus, one of the big four Swiss refineries which used to be owned by the Union Bank of Switzerland (now UBS), had indeed refined several tons of gold from eastern Congo amid a genocide that killed as many as six million people. The refinery was investigated for aiding and abetting in pillage as a war crime on the basis of a complaint presented by the NGO Trial International and material delivered by the United Nations Group of Experts on the DRC. The Attorney General concluded in 2015 that although Argor-Heraeus should have known the origin of the gold (officially declared to originate in Uganda which unlike its neighbour had almost no gold of its own), it did not have actual knowledge. The decision has been criticised as political and raised questions over the line between “turning a blind eye” versus “should have known.”

Murky practices continue

Pieth notes that Switzerland-based refineries today claim that the quantity of problematic gold in their supply chains is negligible even if the risk cannot be entirely excluded. Swiss NGOs such as Public Eye and the Society for Threatened Peoples beg to differ and have done so over multiple reports flagging human rights and environmental issues from Peru to Togo. In his book, Pieth unpacks the problems in the supply chains of refineries Metalor and Valcambi in South America and Africa, highlighting as he goes the limitations of existing due diligence standards and opportunities to interpret existing rules more strictly.

“If only half of what the media and NGOs report is correct, current due diligence standards and especially their implementation needs to be seriously reviewed,” writes Pieth. He believes that Switzerland, home to four of the world’s largest refineries and the importer of up to 70% of the world’s gold, must raise the bar.

Yet the Swiss government has repeatedly been reluctant to adopt stricter regulations on precious metals out of concern for allowing the industry to remain competitive. The main debate about responsible supply chains in Switzerland is whether due diligence requirements need to be made mandatory. This question that could be laid to rest in an upcoming popular vote on the Responsible Business Initiative, which sets out to do just that.

John Williams will discuss why he still believes that hyper inflation will take place even though recent history suggests with so much worldwide debt deflation will prevail.

Jim Willie returns to SGT Report to discuss Trump, geopolitics, the economy and the four facts the show a gold standard, at least three times the current gold price is coming into view.

The data is in: based on a review of reports from multiple consultancies, the silver market has officially entered a supply/demand imbalance.

The structure now in place sets up a scenario where a genuine crunch could occur. Join Mike Maloney and Jeff Clark as they examine the latest startling data.

Clamoring for a rate cut — the first in more than a decade — by the Federal Reserve at some point this year is running hot.

A survey by the Wall Street Journal earlier in the week signaled that nearly 40% of economists (paywall) polled by the publication expect the U.S. central bank to ease monetary policy next month.

The chief economist Joe Davis of Vanguard, the fund provider that manages some $5.4 trillion of wealth, speculated that an “insurance” rate cut by Jerome Powell’s Fed could arrive as early as Wednesday, at the conclusion of the central bank’s two-day policy gathering that kicks off June 18. Federal-funds futures pointed to an 87% chance for a July cut and 26% chance for an easing this month, as of late Friday, CME Group data show.

But what if Wall Street is stone-cold wrong about the Fed cutting, or even communicating its intent to reduce benchmarks rates, which currently stand a range between 2.25%-2.50%, in coming meetings?

Kathy Bostjancic, chief U.S. financial economist at Oxford Economics, told MarketWatch that the domestic economy hasn’t weakened sufficiently to justify dialing back rates.

“The Fed might not be prepared to confirm such validations given the hard data do not yet signal a sharp slowdown in economic activity,” she said.

May’s woeful employment report from the Labor Department, with just 75,000 jobs created on the month, compared with expectations for 185,000, is often cited as evidence of cracks forming in the economy, which is set to mark at the end of this month a record for the length.

However, other data have been relatively healthy if failing to dazzle. A measure of retail sales activity indicated that persistent talk of the demise of the U.S. consumer is overstated. U.S. retail sales gauged by the Commerce Departmentincreased 0.5% in May, slightly below expectations of 0.7%, while the reading for April sales was raised to a 0.3% gain from the initial report of a 0.2% fall.

The University of Michigan’s consumer-sentiment index came in at 97.9 in early June, down from a seasonally adjusted 100 in May but slightly higher than estimates for 97.3, and a measure of industrial production rose 0.4% in May, representing its strongest monthly rise in six months, helped by increased production of pickup trucks and cars.

Those reports don’t immediately scream out for a pre-emptive rate cut, some strategists argue.

However, the data do pose a conundrum for the Fed, which must weigh lowering rates—off already low levels—to curtail the effect of a protracted Sino-American trade conflict even as data remain relatively stable—at least for now. To be sure, the corporate chieftains say trade-war worries are forcing them to rethink their business strategies.

That all sets the stage for a possible disappointment for a market that is pining for rate cuts, betting that the trade friction between the U.S. and China could yield a more dovish, or accommodative, posture from U.S. monetary policy makers, with the 10-year Treasury note TMUBMUSD10Y, +0.21% closing at a paltry 2.093% on Friday, while the S&P 500 SPX, +0.17% is off a mere 2% from its April 30 record and the Dow Jones Industrial Average DJIA, +0.12% is about 2.8% shy of its Oct. 3 all-time high, while the Nasdaq Composite indexes COMP, +0.70% was about 4.5% off its 52-week high. That is notable because the Nasdaq slipped into correction territory, commonly defined as a 10% drop from a recent peak, about two weeks ago...

The policy interest rates of advanced-country central banks are stuck at uncomfortably low levels. And not just for the moment: a growing body of evidence suggests that this awkward condition is likely to persist. Inflation in the United States, Europe, and Japan continues to undershoot official targets. Measures of the “natural” rate of interest consistent with normal economic conditions have been trending downward for years.

Estimates of the natural rate for the US currently put it in the range of 2.25-2.5% – in other words, just where the Federal Reserve’s policy rate is lodged. This means that the Fed has little scope for tightening without missing its inflation target and endangering economic growth. And what is true of the Fed is truer still of the European Central Bank and the Bank of Japan.

This ceiling on the feasible level of interest rates means that when the next recession hits, central banks will have little scope for reducing them. To be sure, certain creative members of the central banking community have experimented with negative interest rates. But scholarly post-mortems suggest that negative rates adversely affect commercial banks’ profitability and weaken the banking system. It follows that risk-averse central bankers will be loath to repeat these experiments.

Thus, when the next recession hits, central banks will again be forced to resort to quantitative easing. QE4, if we can call it that, will elicit howls of protest from the critics of previous rounds of QE, who warned that central banks were exceeding their mandates. By purchasing mortgage-backed securities and corporate bonds, the detractors complained, central banks were distorting financial markets. By engaging in maturity-extension operations, they were destroying the information content of the yield curve. By expanding their balance sheets, they were exposing themselves to the risk of capital losses.

Disapproving politicians questioned whether central bankers could be entrusted to carry out this expanding range of transactions without “adult supervision” by the public’s designated representatives, namely themselves. It followed, as sure as night follows day, that central banks’ independence came under increasingly hostile political attack.

The lesson drawn by those who set great store by central-bank independence is that QE should have been avoided last time and is best avoided in the future, because it opens the door to political interference with the conduct of monetary policy.

But QE’s opponents should consider the alternative. Absent this support from advanced-country central banks following the global financial crisis, a debilitating deflation might have set in, and the post-crisis recession would have been more severe. What would the critics have said then? It seems unlikely that central-bank independence would have survived the even more damning accusation, justified in the event, that monetary policymakers were asleep at the switch.

Another criticism of QE, especially prevalent in Europe, is that it creates moral hazard for governments. Central banks’ purchases of government securities artificially depress the cost of borrowing. Normally, governments issuing additional debt see their borrowing costs rise, which discourages them from overdoing it. In particular, market discipline in the form of higher interest rates will cause a government like Italy’s, tempted to increase deficit spending, to think twice. Not so, however, when the central bank acts as bond buyer of last resort and is prepared to purchase government securities without limit. In such circumstances, market discipline will be incapacitated.

Populist leaders predisposed to ignore budget constraints and promising lavish transfers to their constituents will then have more room to run. The economy will experience an immediate sugar high as a result of the additional public spending, solidifying support for the political incumbents. But, as the American economist Herbert Stein famously observed, something that can’t go on forever ultimately won’t. In the long run, either debt default or debt monetization and inflation will inevitably result from populist profligacy.

It is better, the implication follows, for central banks to resist the siren song of QE. Governments will then feel pressure to live within their means. If populist leaders nevertheless implement their characteristically irresponsible fiscal policies, financial markets will take them to task. If investors sell off massively on the populists’ watch, their political support will collapse.

Again, however, one must consider the alternative. If central banks shun QE in the next downturn, the resulting output collapse will be more severe. Populist politicians, arguing that mainstream leaders and their appointees are not reliable stewards of the economy, will have more evidence to invoke and more anger to channel when they campaign for office. With populists heading more governments, budget deficits will be larger, not smaller. Instability will be greater, not less.

The critics of QE are right to warn of unintended consequences. But shunning QE may have unintended consequences as well. The critics should be careful what they wish for.

Financial writer and precious metals expert Craig Hemke says, “This idea that the Fed can just keep doing what they are doing and things can just keep marching along, no.

We are finally at the end of the charade. It’s lasted a lot longer than I thought it could. Now, in 2019, we are right back to where we were in 2010.

This is vitally important for people to understand. Eventually, gold is going to break out this year. It’s going to go above $1,360 and the whole world is going to figure this out, and prices are going to accelerate. People who are not buying it now are going to get left behind.

Once the demand for all these dollars starts to fall off and disappear, well, those dollars are still out there, and they are all going to come back here to our shores.

That’s when you start to get this runaway or hyperinflation because you’ve got so many more dollars than you have demand for dollars. That lessens the value of the dollar and goods go up in cost. . . . The idea you could get 20% inflation is certainly plausible and feasible.

Nothing has proven more effective in history to preserve wealth than gold and silver—nothing! 2019 will be the best year for precious metals since 2010.”

Richard Maybury, publisher of U.S. & World Early Warning Report for Investors, explains what impact the insane monetary policy will have on our investments.

Bitcoin’s prices have been linked to emerging markets, including the Yuan, and it is unlikely the Chinese currency will move enough to cause investors to flood into bitcoin, this according to Christopher Vecchio, senior currency strategist of DailyFX.com.

“Now, over the past month, the currency with the highest correlation to bitcoin has been the Yuan. The fact that we’ve seen the Chinese Yuan weaken so significantly as these trade wars fears have increased has been that catalyst needed for bitcoin to rally,” Vecchio told Kitco News.

A return to December 2017 highs for bitcoin is unlikely, said Vecchio, as that would imply a Dollar-Yuan rate of past 7, signaling a “world on fire” type of event that necessitates a major escalation of the trade war to a new “realm altogether”.

You can't tax your way to prosperity...but you can surely tax your way into poverty.

Instead of drastically shrinking government involvement in the U.S. economy, and making America more competitive, the Trump Administration chose to increase government intervention.

Tariffs have always been destined to fail. The ramifications are hitting Americans hard, and it looks like it will get even worse!